↑ SEPTA trains connect Philadelphia commuters with nearby regions. Matt Rourke/AP

Richard Florida continues here to characterise the cities that attract start-ups and “creative class” inhabitants

by Richard Florida – 18 July 2019

by Richard Florida – 18 July 2019

Startups Are Abandoning Suburbs for Cities With Good Transit

A new study finds that new business startups are choosing cities with good public transportation options over the traditional suburban locations.

But high-tech startups have become increasingly urban in the past decade or so, gravitating to dense neighborhoods in downtown San Francisco and Lower Manhattan, which have supplanted Silicon Valley as the nation’s leading centers for such startups.

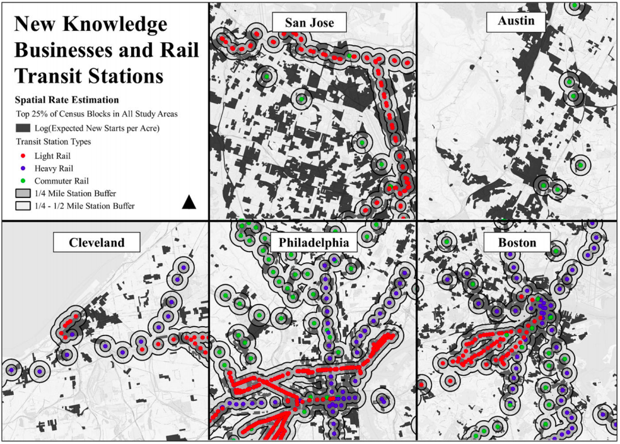

Now a new study finds a close connection between transit access and startups of all types—not just high-tech startups. The study, by Kevin Credit from the Center for Spatial Data Science at the University of Chicago, uses advanced spatial econometric techniques to examine the connection between transit and business startups in five cities. Two of them, San Jose (Silicon Valley) and Austin, are well-documented startup hubs with underdeveloped transit infrastructure; two others, Philadelphia and Cleveland, have reasonably well-developed transit systems but low rates of startup activity; and Boston has both a high level of startup activity and an established transit system.

He tracks startups using detailed data from the National Establishment Time Series (NETS, a private provider of data on U.S. businesses) on location, industry sector, and year of birth, classifying businesses by four industries: retail, services, and food; high-tech; producer services; and a broad knowledge-based category spanning information, finance, real estate, and management. The study calculates the proximity of startups at the block level at 0.25 and 0.5 mile increments from three types of transit: commuter rail, light rail, and heavy rail, in the census blocks for all counties in each Metropolitan Statistical Area (MSA) containing rail transit stations.

The study documents a close relationship between startups and transit, even though the average block in the study has residents with a fairly high level of car ownership (1.74 vehicles per household). The average block also shows relatively high levels of educational attainment among adults with 36 percent holding a college degree.This positive relationship exists “even while controlling for several forms of spatial dependence, total existing and new business activity in the block, and other socio-demographic factors,” the study notes.

But there are clear differences between the five cities, as the maps above show. Light rail systems are shown in red, heavy rail in purple, and commuter rail in green. (For example, Boston’s green line, which began life as an above-surface line is light rail; the rest of its T system, like many underground city systems, is heavy rail; and the MBTA’s broader regional train is commuter rail.) The dark blotches indicate expected startups per acre. You can see the clustering of startups around transit in Philadelphia and Boston for a simple reason: their more established transportation systems. After all, they are the two cities featured in urban historian Sam Bass Warner’s books on the rise of transit-served streetcar suburbs.

Generally speaking, commuter rail stations are the most extensive, with nearly ten percent of all blocks being within a half-mile of a station, compared to only five to six percent of blocks being near any rail stations. As the study notes, “by their nature as ‘commuter’ transit, these rail stations represent generally larger investments (in terms of size and design) and/or tend to be located in more desirable locations for business development, for example, suburban locations.”

The most interesting finding concerns the way different kinds of industries cluster around transit. It’s the least technologically intensive industries—retail, services, and food—that cluster the most around transit. That makes sense, since these businesses tend to locate in and around high-traffic locations to catch the eye of passersby and potential customers. Next in line are the broad knowledge businesses, high-technology, and then producer services. It’s not just high-tech startups that gravitate to transit, it’s all kinds of new businesses.

Ultimately, transit is more than just a mobility strategy, it is a stimulant for new business creation, job generation, and economic development as well.

CityLab editorial fellow Claire Tran contributed research and editorial assistance to this article.

About the Author ![Richard Florida]()

View original article at www.citylab.com

Recent Comments